The greenback tumbled sharply following a disappointing report on December retail sales, pushing the dollar lower against the Aussie to 0.9328 and the Canadian dollar to 1.0225. The December retail sales report missed expectations for an increase of 0.5%, instead declining by 0.3% versus an upwardly revised November reading of 1.8%. The excluding automobiles retail sales figure fell by 0.2% from a 1.9% reading previously. Weekly jobless claims edged up to 444k versus 433k in the previous week.

Economic reports slated for release on Friday include December CPI, Empire manufacturing survey, industrial production, capacity utilization and the University of Michigan consumer confidence survey.

Monday, January 18, 2010

USD Bounces Higher, GBP Slumps

The dollar edged higher against the majors in the Tuesday session, advancing to its highest level since September versus the euro at 1.4216 and a two-month high against the British pound at 1.5920. A barrage of economic reports were released from the US including Q3 GDP, October home prices, November existing home sales, and the December Richmond Fed survey.

Economic growth in the US slowed in the third quarter with GDP downwardly revised to 2.2% from the previous reading of 2.8%. The Q3 GDP deflator was lower at 0.4% from 0.5% previously and PCE prices slipped to 2.6% from 2.7%. Third quarter corporate profits were also downwardly revised to 12.7% compared with 13.4% previously. The key highlight in the data was a strong surge in November existing home sales, which spiked up to 7.4% -- far outpacing estimates for a decline to 2.9% and improving to 6.54 million units. The October home price index improved to 0.6% on a monthly basis and declined by 1.9% on an annualized basis. Meanwhile, the Richmond Fed composite index deteriorated to -4 in December versus a 1.0 reading in the previous month while the services index worsened to -9 from -7.

The calendar for Wednesday includes November PCE, personal income, consumption, the December University of Michigan consumer confidence index, and November new home sales.

Economic growth in the US slowed in the third quarter with GDP downwardly revised to 2.2% from the previous reading of 2.8%. The Q3 GDP deflator was lower at 0.4% from 0.5% previously and PCE prices slipped to 2.6% from 2.7%. Third quarter corporate profits were also downwardly revised to 12.7% compared with 13.4% previously. The key highlight in the data was a strong surge in November existing home sales, which spiked up to 7.4% -- far outpacing estimates for a decline to 2.9% and improving to 6.54 million units. The October home price index improved to 0.6% on a monthly basis and declined by 1.9% on an annualized basis. Meanwhile, the Richmond Fed composite index deteriorated to -4 in December versus a 1.0 reading in the previous month while the services index worsened to -9 from -7.

The calendar for Wednesday includes November PCE, personal income, consumption, the December University of Michigan consumer confidence index, and November new home sales.

China Tightens Policy, JPY Gains

The dollar was lower against the majors in the Tuesday session, sliding to 90.73 against the yen and to just shy of the 1.62-level versus the British pound. The global equity bourses also slumped, with the S&P500 and Nasdaq lower by over 1% while Dow Jones slipped by around 0.7% in afternoon trading. Meanwhile, spot gold was down by nearly 2% to $1,129.60 per ounce and WTI crude oil slipped by around 2.3% to $80.65 per barrel.

The economic calendar from the US was light, with just the release of the November trade deficit. The US deficit was slightly less than expected at $33.2 billion, versus a revised $32.9 billion from October. The data for the latter part of the week will include on Thursday: December retail sales, weekly jobless claims, November business inventories and on Friday: December real earnings, core CPI, CPI, industrial production, capacity utilization, January NY Fed manufacturing index, and the University of Michigan consumer confidence survey.

The key catalyst in market moves today largely stemmed from an unexpected change in policy from China. The PBOC surprised markets by raising the reserve requirements by 50-basis points overnight, effective January 18th. The move is aimed to cool down China’s economy, preventing it from overheating and preempting inflationary concerns. The move will likely be followed by further action over the coming months, in line with expectations for a global tightening of monetary policy as well – with the RBA the next likely central bank to hike interest rates again.

The economic calendar from the US was light, with just the release of the November trade deficit. The US deficit was slightly less than expected at $33.2 billion, versus a revised $32.9 billion from October. The data for the latter part of the week will include on Thursday: December retail sales, weekly jobless claims, November business inventories and on Friday: December real earnings, core CPI, CPI, industrial production, capacity utilization, January NY Fed manufacturing index, and the University of Michigan consumer confidence survey.

The key catalyst in market moves today largely stemmed from an unexpected change in policy from China. The PBOC surprised markets by raising the reserve requirements by 50-basis points overnight, effective January 18th. The move is aimed to cool down China’s economy, preventing it from overheating and preempting inflationary concerns. The move will likely be followed by further action over the coming months, in line with expectations for a global tightening of monetary policy as well – with the RBA the next likely central bank to hike interest rates again.

Dollar Slides vs Major FX

The dollar was broadly lower against the major currencies in the first trading day of 2010, relinquishing the 1.44-level versus the euro and sliding to 1.0374 against the Canadian dollar. Crude oil popped back above the $80 per barrel level while the global equity bourses advanced in the Monday session as traders shifted back into riskier assets. The Dow Jones, Nasdaq and S&P 500 were all higher by over 1.5% by afternoon.

The economic calendar was light today, with the release of the December manufacturing ISM report. The data improved by more than expected, edging up to 55.9 and beating calls for an increase to 54.0 from 53.6 in November. The ISM prices paid component jumped to 61.5 versus 55.0 in the previous month.

The week ahead will see a barrage of reports including November durable goods orders, pending home sales, factory orders, December non-manufacturing ISM, ADP private sector payrolls, weekly jobless claims and the key December jobs report. The non-farm payrolls for December are seen worsening to -20k from -11.0k from a month earlier, while the unemployment rate is expected to edge up slightly to 10.1% from 10.0% from November.

The economic calendar was light today, with the release of the December manufacturing ISM report. The data improved by more than expected, edging up to 55.9 and beating calls for an increase to 54.0 from 53.6 in November. The ISM prices paid component jumped to 61.5 versus 55.0 in the previous month.

The week ahead will see a barrage of reports including November durable goods orders, pending home sales, factory orders, December non-manufacturing ISM, ADP private sector payrolls, weekly jobless claims and the key December jobs report. The non-farm payrolls for December are seen worsening to -20k from -11.0k from a month earlier, while the unemployment rate is expected to edge up slightly to 10.1% from 10.0% from November.

Saturday, January 16, 2010

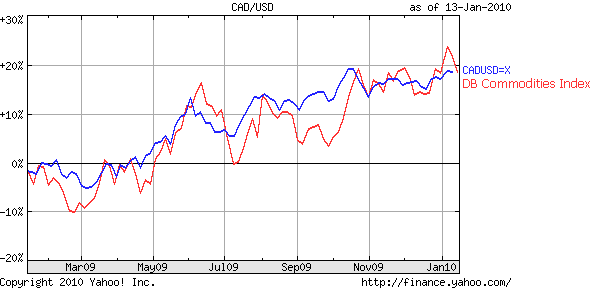

Canadian Dollar Headed for Parity

Only a year ago, who could have conceived of such a possibility? At the time, the Canadian Dollar (aka Loonie) was in the doldrums, as a result of the credit crunch and concomitant collapse in commodity prices. In March, however, the Loonie began an extraordinary rally, and finished the year up 16%, almost perfectly offsetting the record decline that it suffered in 2008. As a result, the Loonie is now only pennies away from returning to parity.

The Loonie’s rise can be ascribed to a combination of fundamentals and speculation. On the fundamental side, a surge in the price of oil and other commodities has driven a recovery in the Canadian economy. Summarized one strategist, “The fundamentals in Canada are strong. Sentiment is bullish Canada, and on a relative basis, Canada should do very well with stronger commodity prices and ongoing U.S. economic recovery.” On the other hand, non-commodity exports remain sluggish, such the current account balance is currently in the red.

It’s obvious then that the gap between reality and expectation is being filled by speculation. Despite the fact that both short-term and long-term Canadian interest rates remain low, investors are pouring money into Canadian assets in the hopes that rates will soon rise. This speculation reached a fever pitch in October of 2009, when the Loonie spiked 6% in less than two weeks, following a modest Australian rate hike.

At that point, Canadian Central Bank governor Mark Carney was forced to firmly step in (previously he had effectively remained on the sidelines) by warning investors that he was in no hurry to lift rates, and that “he had ways of cooling the currency.” While analysts credit Carney’s jawboning with effecting a modest decline in the Loonie, it has since resumed its upward march, breaking through the technical barrier of 97.5 CAD/USD yesterday.

In the short-term, sheer momentum will almost surely carry the Loonie through parity with the Dollar. Analysts are divided on the timing, with some suggesting as soon as this month and others suggesting that later in the year is more likely. They should be careful, as there is an exuberance in the forex markets that I havn’t seen since right before Lehman Brothers collapsed- the event that many say signaled the beginning of the forex markets. In other words, investors are surely getting ahead of themselves, since commodities are well off of their 2008 highs, interest rates are down, Canadian economic growth is mediocre, Canada’s fiscal condition is weak, and it is operating a current account deficit.

For this reason, many analysts are already becoming bearish on the Loonie. “The loonie looks potentially more vulnerable on a number of crosses unless we see renewed upside momentum,” expressed a strategist from RBC Capital Markets. But noticed that she framed a continued rise in terms of momentum, rather than fundamentals. That’s tantamount to saying, Unless the Canadian Dollar continues to appreciate, it won’t continue to appreciate. If that’s not a tautology, I don’t know what is! But seriously, she has a point, which is that the Loonie is being driven purely by speculation at this point, in a trade that could soon come crashing down…after it hits parity.

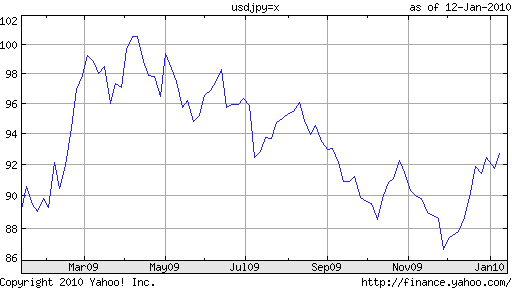

Making Sense of the Yen: Forex Intervention, Debt and Deflation

Last week, Hirohisa Fujii resigned as finance minister of Japan. Since Fujii was anoutspoken commentator on the Japanese Yen, the move sent a jolt through forexmarkets. Those who were expecting that his replacement, Deputy Prime Minister Naoto Kan, would be be more consistent than his predecessor were quickly disappointed, as Mr. Kan managed to contradict himself repeatedly within days of assuming his new post.

On January 6, he said it would be “nice” to see the Yen weaken, going so far as to designate 95 Yen/Dollar as the level he had in mind. One day later, he said that the markets should in fact determine the Yen: “If currency levels deviate sharply from the estimates, that could have various effects on the economy.” After he wasrebuked by Prime Minister Yukio Hatoyama, who noted that the government should not talk to reporters about forex, he went on tell US Treasury Secretary that forexlevels should be stable. In short, Japan’s official governmental position on the Yen still remains muddled, and it’s no less clear whether it will – or even should – intervene.

Fortunately, they may not have to. Not only because the Yen still remains more than 5% off of the record highs of November, but also because economic and financial forces are coalescing that could send the Yen downward. Despite a recovery in exports, the Japanese economy remains beleaguered, having most recently contracted to the lowest level since 1991, as part of a “tumble [that] isunprecedented among the biggest economies.” Now that we are into 2010, it can be said officially that Japan has now suffered from the “second lost decade in a row.”

When economic growth collapsed in 1990, Japanese consumers became famously frugal, and the domestic market still hasn’t recovered. Neither has the stock market, for that matter: “The Nikkei is 44.3% below where it stood at the end of 1999. It is 72.9% below its peak near the end of 1989.” The performance of the bond market, meanwhile, has been a mirror image, rallying 78% since 1990.

The resulting decline in real interest rates has combined with economic stagnation to produce a perennial state of deflation. In fact, prices are once again falling, this time by an annualized pace of 2%.

As many economists have been quick to diagnose, the problem lies in a tremendous (perhaps the world’s largest) imbalance between savings and investment, as “Japan still has ¥1,500 trillion ($16.3 trillion) of savings.” It’s not clear how long this can last, however, as Japanese demographic changes tax the nation’s pool of savings. “More than a fifth of Japanese are over 65…The nation’s population began shrinking in 2006 from 127.8 million, and will drop by 3.2 percent in the coming decade.”

This brings me to the final component of Japan’s perfect economic storm: debt. Japan’s gross national debt is projected by the IMF to touch 225% of GDP this year, and 250% as early as 2014. As a result of the aging population, the pool of cash available for lending to the government is shrinking at the same rate as the tax base, which is exerting fiscal pressure on the government from both sides. According to one commentator, “Japan’s fiscal conditions are close to a melting point.” Another frets: “I doubt there is any yield that international capital markets can find acceptable that will not bankrupt the Japanese state.”

What is the government doing about all of this? Frankly, not too much. It is spending money like crazy – exacerbating its fiscal state and pushing it closer to insolvency – in a (vain) attempt to prime the economic pump and avoid deflation from further entrenching. The Central Bank, meanwhile, just announced a new round of quantitative easing, also aimed at fighting deflation. At only 2% of GDP, however, the measures are “pretty tame” and unlikely to accomplish much. Considering that its monetary base has only expanded by 5% this year (compared to 71% in the US), it still has plenty of scope to operate. At the present time, however, it is still reluctant to do so.

Ironically, the aging population phenomenon could end up restoring Japan’s economy to equilibrium. The worse Japan’s fiscal problems become, the sooner it will be forced to simply print money, so as to deflate its debt and avoid default. This will stimulate the economy and put upward pressure on prices (solving two problems), and exert strong downward pressure on the Yen. The way I see it, that’s four birds with one stone!

As for the Yen, then, I would expect it to hover over the near-term, since price stability and a strong credit rating don’t signal immediate catastrophe. No, Japan’s economic problems are more long-term, which means it could be a while before they more clearly manifst themselves.

Chinese RMB Set to Appreciate in 2010

The Chinese Yuan (RMB) spent all of 2009 pegged to the Dollar at 6.83. Since the Dollar depreciated against almost every other currency during that time period, the Yuan has fallen against these currencies, undoing most of its appreciation in 2008. As a result of both international pressure and internal economic conditions, however, the Yuan’s stasis should come to an end soon. The only questions are when, howand to what extent.

In hindsight, the Central Bank (i.e. state economic planners) of China were probably justified in holding the Yuan in 2008. At a time when forex markets (and other capital markets, for that matter) were behaving erratically, the Yuan was a baston of stability. China’s premier, Wen Jiabao, recently boasted, “Keeping the yuan’s value basically steady is our contribution to the international community at a time when the world’s major currencies have been devalued.” In fact, there is evidence that the Central Bank went against market forces in the opposite direction during the height of the credit crisis, and successfully prevented the Yuan from depreciating, thus proving that a currency peg can work both ways. The result was price stability, and a boost to exporters that had been damaged by the falloff in foreign demand for Chinese goods.

With the global economy emerging from recession, the argument for maintaining the peg is becoming less tenable. China’s economy, itself, grew at an impressive 8.5% in 2009, and is forecast to grow even faster in 2010, by 9.5%. Thanks to a surge in bank lending and the government’s massive economic stimulus program, inflation is also ticking up. It has been approximated at 2.5%, but is contradicted by spikes of 50%+ in the prices of certain staple goods, and certainly doesn’t take into account the rise in asset prices. China’s benchmark stock market index surged 90% in 2009, and property prices increased by 30% in some areas.

The dual concerns, of course, are that the money supply is expanding too fast and that bubbles are forming in certain asset markets. The weak RMB is certainly not helping either. Thanks to relaxed capital market controls and expectations of further appreciation, speculative “hot money” is once again pouring into China. Holding down the Yuan in the face of such pressure is becoming prohibitivel expensive: “China’s foreign-exchange reserves climbed 17 percent in the first nine months of 2009 to $2.27 trillion, the world’s largest holdings.” Some of the demand is naturally beingtempered by bubble concerns, but the trend is still money coming into China.

There is also the argument, much mooted in economics circles, that an appreciation of the RMB would be good for the Chinese economy. Because of a perennially weak currency, its economy has become to addicted to exports to drive growth. “As a report from research firm Euromonitor International notes, in U.S. dollar terms,China’s consumer market lags those of the U.S., Japan and much of Europe, with private consumption just over one third of GDP in 2008.” This is probably a product of social and cultural forces, which still emphasize saving. Skeptics of the usefulnes of RMB appreciation point out that rebalancing the Chinese economy would start with changing the culture of saving, but a stronger currency would certainly provide a powerful incentive. Not to mention that a more valuable RMB would give Chinese companies more leverage in consummating outbound corporate M&A deals and natural resource acquisitions that they have been so keen on in recent years.

On the other side of the debate are skeptics of a different sort- those that think RMB appreciation is justified by forward-looking macroeconomic fundamentals. Some fear hyperinflation of the sort that China faced in 2007 and was only brought under control by the global economic recession and concomitant decline in resource prices. “Franklin Allen, a professor of finance at Wharton [University of Pennsylvania], estimates the likelihood of inflation reaching between 10% and 20% to be around one in five.” Any inflation beyond what is experienced in other economies would have to be reflected in the RMB. In a hyperinflation scenario, the Central Bank might even have to deliberately depreciate the currency.

Then there are the skeptics that forecast an economic crash in China. James Chanos, a wealthy hedge fund manager is leading this chorus, “warning that China’s hyperstimulated economy is headed for a crash, rather than the sustained boom that most economists predict. Its surging real estate sector, buoyed by a flood of speculative capital, looks like “Dubai times 1,000 — or worse.’ ”

While this view is gaining some traction, it is still relegated to the minority. Investors and economists are now operating under the firm assumption that China will allow the RMB to resume its appreciation soon. As for when, it could be any day, though probably not for a few months still. As for the questions of how and to what extent, some economists have argued for a one-off appreciation (10% has been suggested)in order to discourage future inflows of speculative capital. Most analysts, though, expect the rise to be gradual. Futures prices currently reflect a 3% rise over the next year, and the consensus among economists is similar. It also depends on how the Dollar performs over the near-term: “If better-than-expected growth in the U.S. helps the greenback recover this year…That would take some of the pressure off Chinese policy makers.”

Subscribe to:

Posts (Atom)